Wash Sales

A wash sale occurs when you sell a security at a loss and then purchase that same security within 30 days (before or after the sale date).

Your loss will be disallowed and added to the cost basis of the securities you repurchased. Thus "deferred" might be a better term to use than "disallowed".

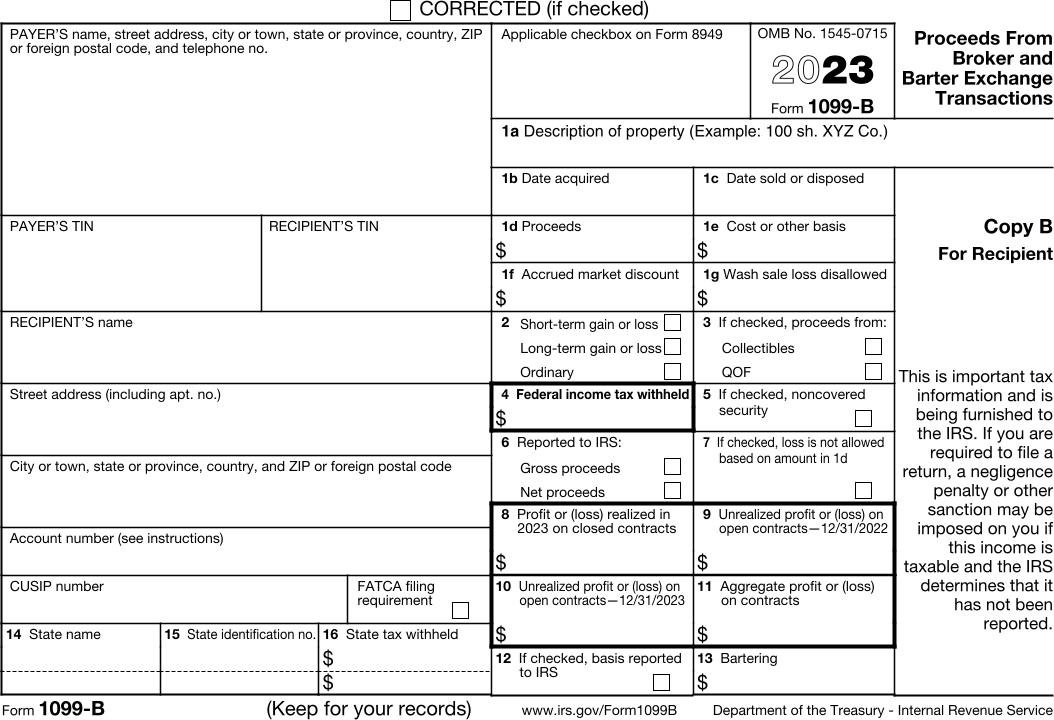

IRS regulations require that a broker track and report wash sales on the same CUSIP number (a unique nine-character identifier for a security) within the same account.

Wash sale loss disallowed is reported in Box 1g.

Cost or other basis, Box 1e, includes any deferred wash sale losses that were added to the cost of repurchased shares.

Articles and Information

- https://www.irs.gov/publications/p550#en_US_2017_publink100010601

- https://en.wikipedia.org/wiki/Wash_sale

- https://www.investopedia.com/terms/w/washsale.asp

- https://www.investopedia.com/terms/w/washsalerule.asp

- https://www.schwab.com/resource-center/insights/content/a-primer-on-wash-sales

Why our app does not compute wash sale adjustments

Starting in 2011 the IRS began requiring brokers to determine cost and wash sale loss adjustments and disclose those amounts on Form 1099-B. Determination of cost requires buy/sell matching, accounting for options transactions, and corporate actions such as splits. Wash sale accounting follows cost determination. In that year we made the decision to not redo the work already done by brokers. We start with broker 1099-B data and generate Form 8949 and Schedule D from that data.

If you need to do wash sale accounting, consider https://www.tradelog.com/

In our opinion, in some cases, the cost to comply with the "letter of the law", coupled with the small difference it makes in your taxes, is such that compliance does not make sense. Use your own discretion.